If you were injured as a passenger in a Florida car accident, you can bring a claim against any driver whose negligence caused the crash — the driver of the car you were in, the driver of the other vehicle, or both. Your own PIP (Personal Injury Protection) coverage typically pays your first medical bills, and you may also recover through bodily injury liability coverage, uninsured motorist (UM) coverage, or claims against third parties such as a vehicle’s owner or a negligent driver’s employer. Passengers are almost never at fault, which usually makes their liability claims stronger than a driver’s.

Key Takeaways

- Passengers can sue one or both drivers. Fault is divided between them under Florida’s comparative fault law (Fla. Stat. § 768.81).

- Your own PIP usually pays first — even in someone else’s car — under Fla. Stat. § 627.736. Seek medical care within 14 days or lose PIP benefits.

- Suing a friend or relative is really an insurance claim. Their insurer — not their savings — defends and pays the claim up to policy limits.

- Florida does not require bodily injury coverage, so UM/UIM coverage is often the difference between full recovery and nothing.

- You generally have 2 years to file suit for crashes on or after March 24, 2023 (Fla. Stat. § 95.11, as amended by HB 837).

You trusted someone with the driver’s seat — a friend, a spouse, a rideshare driver — and now you’re the one in a hospital bed. Passengers hurt in Florida car accidents often feel stuck: you didn’t cause the crash, you can’t control the insurance process, and the person most obviously responsible may be someone you care about. The good news is that Florida law treats injured passengers well. Because you were not behind the wheel, you are almost never assigned fault, and you may have more sources of compensation available than either driver does.

This guide from MANGAL, PLLC — a Florida personal injury law firm based in Clermont with an Orlando office — walks through exactly who an injured passenger can sue, whose insurance pays and in what order, and the deadlines that now apply under Florida’s 2023 tort reform law.

Why Passenger Injury Claims Are Different (and Often Stronger)

In a typical two-driver crash, each driver points at the other, and the case becomes a fight over percentages of fault. A passenger sits outside that fight. Unless you did something unusual — grabbed the wheel, distracted the driver, or knowingly got in the car with someone obviously impaired — no one can credibly argue you caused the collision.

That has three practical consequences:

- Liability is rarely disputed against you. The insurers may fight about which driver was at fault, but someone’s insurer almost always owes you.

- You can claim against multiple policies. Both drivers’ bodily injury coverage, the host vehicle’s PIP, your own PIP, and UM coverage can all be in play for a single crash.

- Comparative fault rarely reduces your recovery. Under Fla. Stat. § 768.81, damages are reduced by your percentage of fault — and a passenger’s percentage is usually zero.

The trade-off is complexity. Passenger claims involve more policies, more adjusters, and more coordination-of-benefits questions than a straightforward driver claim. Getting the order of recovery right is where cases are won or quietly lost.

Step One: PIP Pays First — But Whose PIP?

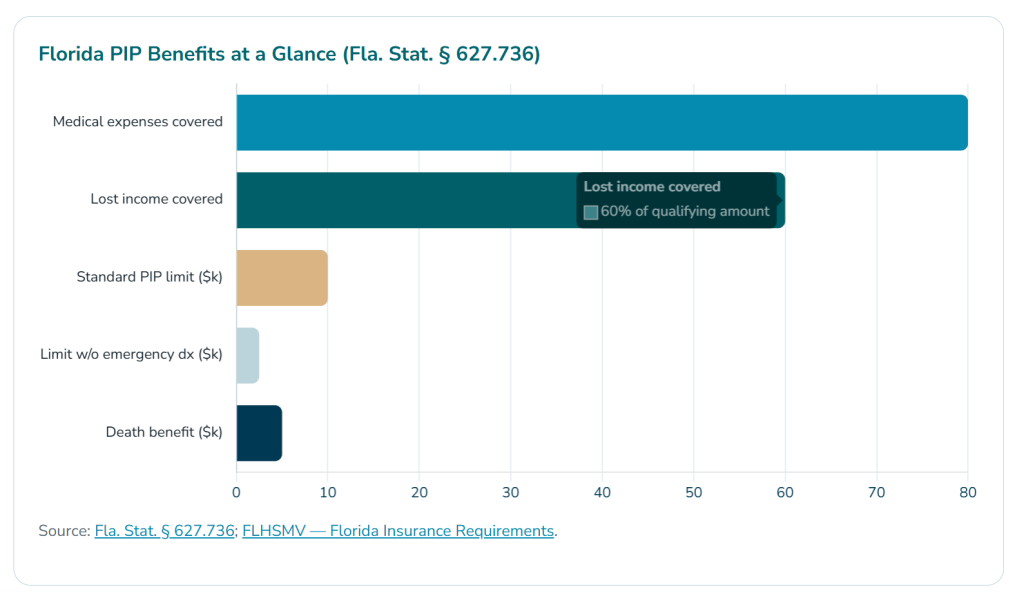

Florida is a no-fault state. Before anyone sues anyone, Personal Injury Protection (PIP) benefits pay initial medical bills and lost wages regardless of fault under Fla. Stat. § 627.736. For passengers, the most common surprise is whose PIP applies. The statute sets a priority order:

The PIP priority order for passengers

- Your own policy. If you own a motor vehicle registered in Florida and carry PIP, your own coverage pays first — even though you were riding in someone else’s car and even though you did nothing wrong.

- A resident relative’s policy. If you don’t own a vehicle but live with a family member who has PIP, their policy generally covers you.

- The host vehicle’s policy. If neither of the above applies, the PIP covering the car you occupied pays your benefits.

What PIP actually pays

- 80% of reasonable medical expenses, up to the coverage limit;

- 60% of lost income;

- a standard limit of $10,000 — reduced to $2,500 if a qualified provider does not diagnose an “emergency medical condition”; and

- a $5,000 death benefit.

The 14-day rule: PIP benefits are available only if you receive initial medical care within 14 days of the crash. Passengers who “wait to see if it gets better” routinely forfeit $10,000 in no-fault benefits. Get examined promptly, even if you feel only sore.

PIP is only a floor. A serious injury exhausts $10,000 in a single emergency room visit — the real recovery usually comes from the liability claims discussed next.

Every Party an Injured Passenger May Be Able to Sue in Florida

“Who do I sue?” usually has more than one correct answer. Below is the full map of potentially liable parties. In most cases, “suing” begins as an insurance claim, and a lawsuit is filed only if the insurer won’t pay fairly.

| Potentially Liable Party | Legal Basis | Insurance That Typically Pays |

|---|---|---|

| Driver of the car you were in | Negligent driving (speeding, distraction, impairment) | That driver’s bodily injury (BI) liability coverage |

| Driver of the other vehicle | Negligent driving | The other driver’s BI coverage |

| Both drivers | Shared fault apportioned under § 768.81 | Both BI policies, in proportion to fault |

| Owner of either vehicle (if not the driver) | Florida’s dangerous instrumentality doctrine — owners are vicariously liable for drivers they entrust | The owner’s auto policy |

| A driver’s employer | Vicarious liability / negligent hiring if the driver was working | Commercial auto or business liability policy |

| Rideshare company coverage (Uber/Lyft trips) | Statutory TNC insurance requirements (Fla. Stat. § 627.748) | Up to $1 million in third-party liability while a ride is engaged |

| A vehicle or parts manufacturer | Product liability (defective airbags, tires, seatbacks) | Manufacturer’s liability insurance |

| A bar or alcohol vendor (narrow cases) | Fla. Stat. § 768.125 — serving minors or persons habitually addicted | Liquor liability coverage |

| A government entity (road defects, government drivers) | Negligence, subject to sovereign immunity limits (Fla. Stat. § 768.28) | Self-insurance; statutory caps and pre-suit notice apply |

Scenario 1: The driver of your car was at fault

You bring a bodily injury claim against your own driver’s liability coverage. This is the situation that makes passengers hesitate — see the friend-and-family section below — but legally it is the most straightforward claim there is.

Scenario 2: The other driver was at fault

Your claim runs against the other driver’s BI coverage, exactly as if you had been the injured driver — except without any comparative-fault argument against you. Evidence like the crash report matters here; our guide on how to obtain a Florida crash report explains the process.

Scenario 3: Both drivers share fault

This is where passengers have a structural advantage. Suppose a jury finds your driver 30% at fault and the other driver 70% at fault. You may recover 30% of your damages from your driver’s insurer and 70% from the other — 100% in total, because none of the fault belongs to you. Fault fights between two insurers are common in intersection accidents, and passengers should never wait on the sidelines while the two carriers argue.

Scenario 4: A commercial vehicle or truck was involved

If either vehicle was a working truck, delivery van, or company car, the employer’s commercial policy — often with far higher limits — may respond. Commercial cases follow different rules and evidence timelines; see our overview of who is liable in a Florida truck accident and our truck accident practice page.

“I Don’t Want to Sue My Friend”: What a Claim Against Your Driver Really Means

This is the number-one reason injured passengers delay — and the biggest misconception in passenger cases.

A bodily injury claim against your driver is, in practice, a claim against their insurance company. The insurer hires the lawyers, handles the negotiation, and pays the settlement up to the policy limits your friend already paid premiums for.

Your friend’s role is usually limited to reporting the crash to their insurer and perhaps giving a recorded statement. Their rates are affected by the at-fault accident itself — which the insurer already knows about — not by whether you fairly claim the benefits that coverage exists to provide. Declining to file doesn’t protect your friend; it only transfers the cost of their mistake onto you, your health insurance, and your family.

Where genuine personal exposure can arise is when injuries exceed policy limits. An experienced attorney structures the claim — including UM coverage and other policies — to maximize recovery within available insurance first.

Not Sure Which Policies Apply to You?

Attorney Avnish Mangal personally reviews every case — and coverage questions cost you nothing to ask. MANGAL, PLLC is available 24/7 and charges no fee unless we win.

Or call (352) 995-9945

The “Serious Injury” Threshold: When a Passenger Can Sue for Pain and Suffering

Because Florida is a no-fault state, Fla. Stat. § 627.737 limits lawsuits for non-economic damages (pain, suffering, mental anguish, loss of enjoyment of life) to cases involving:

- significant and permanent loss of an important bodily function;

- permanent injury within a reasonable degree of medical probability;

- significant and permanent scarring or disfigurement; or

- death.

Economic damages — medical bills beyond PIP, lost wages, future care — can be pursued without meeting the threshold. Whether an injury is “permanent” is a medical question answered through proper diagnosis and documentation, which is another reason early treatment matters. Passengers with soft-tissue injuries that later reveal disc herniations or nerve damage should not let an adjuster label their case “minor” in week one.

Policy Limits and the Multi-Passenger Problem

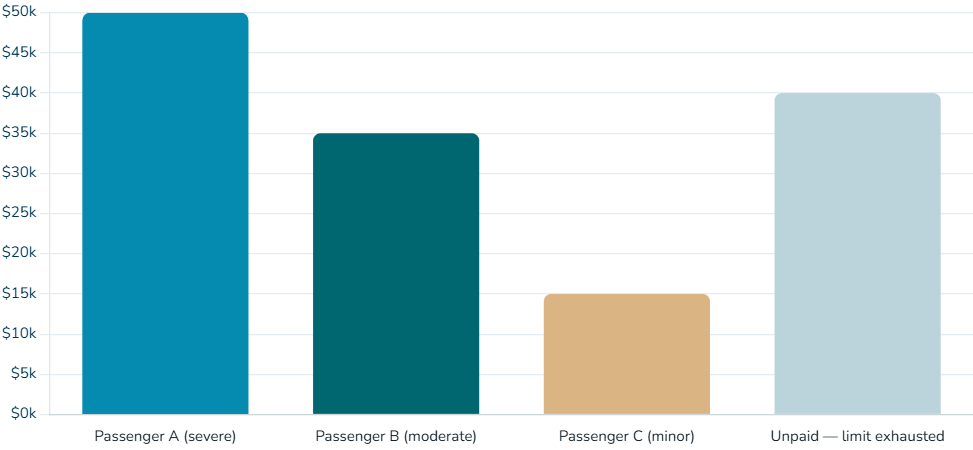

Bodily injury coverage is written with two numbers — for example, $50,000/$100,000: up to $50,000 per injured person, and $100,000 total per accident. When a crash injures a driver and three passengers, all claims share that per-accident pool.

Three practical rules follow:

- Speed matters. Insurers may settle early claims first; late claimants can find the per-accident limit exhausted.

- Every policy must be found. Owner policies, employer policies, umbrella policies, resident-relative UM — passengers frequently leave six figures unclaimed because no one mapped the full coverage picture.

- Proportionality is negotiable. How a shared limit is divided among claimants is not automatic; representation affects your share.

Uninsured Motorist Coverage: The Passenger’s Safety Net

Here is the fact that surprises almost everyone: Florida does not require most private drivers to carry bodily injury liability insurance at all. The state’s minimum requirements are $10,000 PIP and $10,000 property damage liability — see the FLHSMV insurance requirements page. If the at-fault driver has no BI coverage, there may be no liability policy to claim against.

That’s what uninsured/underinsured motorist (UM/UIM) coverage under Fla. Stat. § 627.727 is for. As a passenger you may have access to:

- the host vehicle’s UM coverage (passengers are typically insureds under the policy of the car they occupy);

- your own UM coverage, if you carry it on your policy; and

- a resident relative’s UM coverage, in many circumstances.

UM claims are still adversarial — your own insurer stands in the shoes of the uninsured driver and can dispute the claim just as hard. But layered correctly, UM coverage often rescues cases that would otherwise be uncollectible.

Can a Passenger Ever Be Blamed? The Two Defenses Insurers Try

Passengers start near zero percent fault, but insurers raise two arguments:

1. The seatbelt defense

Florida recognizes failure to wear an available, operational seatbelt as comparative negligence that can reduce damages attributable to that failure. Seatbelt use is also simply the difference between injury categories: the National Highway Traffic Safety Administration reports that seatbelts reduce the risk of fatal injury to front-seat occupants by about 45% (NHTSA — Seat Belts).

2. “You knew the driver was impaired”

Knowingly riding with an obviously intoxicated driver can support a comparative fault argument. It does not bar recovery — under Florida’s modified comparative negligence standard, Fla. Stat. § 768.81(6), a claimant recovers as long as they are not more than 50% at fault, with damages reduced by their percentage. A passenger rarely approaches that bar, but these arguments are exactly what insurers use to discount settlements — and exactly what an attorney is for.

Deadlines: HB 837 Cut the Time to Sue in Half

Florida’s 2023 tort reform law, HB 837, reduced the statute of limitations for negligence claims from four years to two years for causes of action accruing on or after March 24, 2023 (Fla. Stat. § 95.11; see our complete guide to HB 837 and our explainer on the new car accident lawsuit deadline).

- Negligence claims (most passenger cases): generally 2 years from the crash date.

- Wrongful death: 2 years.

- Claims against government entities: pre-suit written notice requirements under Fla. Stat. § 768.28 apply before suit can proceed.

- PIP: initial treatment within 14 days; claims and disputes on much shorter clocks.

Two years sounds like a long time. It is not — especially in multi-policy passenger cases where coverage investigation, medical documentation, and pre-suit negotiation all have to happen first.

Injured as a Passenger? Do These Six Things Now

- Get medical care within 14 days — sooner if symptoms exist. This preserves PIP and documents causation.

- Get the crash report. Both drivers’ insurance details appear on it. (How to get a Florida crash report.)

- Identify every policy: both drivers’ BI, vehicle owners’ policies, your PIP, household UM, employer coverage if applicable.

- Do not give recorded statements to any liability insurer before speaking with counsel — including your friend’s insurer.

- Preserve evidence: photos, dashcam footage, witness contacts, your seat position, and all medical records.

- Talk to a Florida injury attorney early. Coverage priority mistakes made in the first weeks are the hardest to undo.

How MANGAL, PLLC Helps Injured Passengers

MANGAL, PLLC is a plaintiff-side car accident and personal injury firm founded in 2018, headquartered in Clermont with an Orlando office available by appointment, serving passengers injured anywhere in Florida. Attorney Avnish K. Mangal, Esq. — a Cornell Law School graduate and former Vault 100 Manhattan firm associate with a finance background — personally handles every case, regardless of size. The firm is voted #1 Personal Injury Law Firm in Central Florida, is 5-star rated on Google and Avvo, has been trusted by more than 1,000 clients, and answers 24/7.

Passenger cases are coverage puzzles, and Attorney Mangal’s insurance and financial background is built for exactly that: finding every policy, sequencing every claim, and refusing to let two insurers turn their fault fight into your unpaid bills.

Three practical rules follow:

- Speed matters. Insurers may settle early claims first; late claimants can find the per-accident limit exhausted.

- Every policy must be found. Owner policies, employer policies, umbrella policies, resident-relative UM — passengers frequently leave six figures unclaimed because no one mapped the full coverage picture.

- Proportionality is negotiable. How a shared limit is divided among claimants is not automatic; representation affects your share.

Uninsured Motorist Coverage: The Passenger’s Safety Net

Here is the fact that surprises almost everyone: Florida does not require most private drivers to carry bodily injury liability insurance at all. The state’s minimum requirements are $10,000 PIP and $10,000 property damage liability — see the FLHSMV insurance requirements page. If the at-fault driver has no BI coverage, there may be no liability policy to claim against.

That’s what uninsured/underinsured motorist (UM/UIM) coverage under Fla. Stat. § 627.727 is for. As a passenger you may have access to:

- the host vehicle’s UM coverage (passengers are typically insureds under the policy of the car they occupy);

- your own UM coverage, if you carry it on your policy; and

- a resident relative’s UM coverage, in many circumstances.

UM claims are still adversarial — your own insurer stands in the shoes of the uninsured driver and can dispute the claim just as hard. But layered correctly, UM coverage often rescues cases that would otherwise be uncollectible.

Can a Passenger Ever Be Blamed? The Two Defenses Insurers Try

Passengers start near zero percent fault, but insurers raise two arguments:

1. The seatbelt defense

Florida recognizes failure to wear an available, operational seatbelt as comparative negligence that can reduce damages attributable to that failure. Seatbelt use is also simply the difference between injury categories: the National Highway Traffic Safety Administration reports that seatbelts reduce the risk of fatal injury to front-seat occupants by about 45% (NHTSA — Seat Belts).

2. “You knew the driver was impaired”

Knowingly riding with an obviously intoxicated driver can support a comparative fault argument. It does not bar recovery — under Florida’s modified comparative negligence standard, Fla. Stat. § 768.81(6), a claimant recovers as long as they are not more than 50% at fault, with damages reduced by their percentage. A passenger rarely approaches that bar, but these arguments are exactly what insurers use to discount settlements — and exactly what an attorney is for.

Deadlines: HB 837 Cut the Time to Sue in Half

Florida’s 2023 tort reform law, HB 837, reduced the statute of limitations for negligence claims from four years to two years for causes of action accruing on or after March 24, 2023 (Fla. Stat. § 95.11; see our complete guide to HB 837 and our explainer on the new car accident lawsuit deadline).

- Negligence claims (most passenger cases): generally 2 years from the crash date.

- Wrongful death: 2 years.

- Claims against government entities: pre-suit written notice requirements under Fla. Stat. § 768.28 apply before suit can proceed.

- PIP: initial treatment within 14 days; claims and disputes on much shorter clocks.

Two years sounds like a long time. It is not — especially in multi-policy passenger cases where coverage investigation, medical documentation, and pre-suit negotiation all have to happen first.

Injured as a Passenger? Do These Six Things Now

- Get medical care within 14 days — sooner if symptoms exist. This preserves PIP and documents causation.

- Get the crash report. Both drivers’ insurance details appear on it. (How to get a Florida crash report.)

- Identify every policy: both drivers’ BI, vehicle owners’ policies, your PIP, household UM, employer coverage if applicable.

- Do not give recorded statements to any liability insurer before speaking with counsel — including your friend’s insurer.

- Preserve evidence: photos, dashcam footage, witness contacts, your seat position, and all medical records.

- Talk to a Florida injury attorney early. Coverage priority mistakes made in the first weeks are the hardest to undo.

How MANGAL, PLLC Helps Injured Passengers

MANGAL, PLLC is a plaintiff-side car accident and personal injury firm founded in 2018, headquartered in Clermont with an Orlando office available by appointment, serving passengers injured anywhere in Florida. Attorney Avnish K. Mangal, Esq. — a Cornell Law School graduate and former Vault 100 Manhattan firm associate with a finance background — personally handles every case, regardless of size. The firm is voted #1 Personal Injury Law Firm in Central Florida, is 5-star rated on Google and Avvo, has been trusted by more than 1,000 clients, and answers 24/7.

Passenger cases are coverage puzzles, and Attorney Mangal’s insurance and financial background is built for exactly that: finding every policy, sequencing every claim, and refusing to let two insurers turn their fault fight into your unpaid bills.

Frequently Asked Questions: Passenger Injury Claims in Florida

Can a passenger sue the driver of the car they were in?

Yes. If your driver caused or contributed to the crash, you can bring a bodily injury claim against them — even a friend or relative. In practice the claim is presented to and paid by their auto insurer, up to policy limits.

Whose PIP covers me as a passenger?

Your own PIP pays first if you own a Florida-registered vehicle. If you don’t, a resident relative’s PIP may apply; otherwise, the PIP on the vehicle you occupied pays. Remember the 14-day treatment rule under Fla. Stat. § 627.736.

Can I sue both drivers?

Yes. Where fault is shared, each driver’s insurer is responsible for that driver’s percentage of fault under Fla. Stat. § 768.81 — and because none of the fault is yours, you can pursue full compensation across both policies.

What if the at-fault driver has no bodily injury insurance?

Common in Florida, which doesn’t require BI coverage for most drivers. Look to UM/UIM coverage: the host vehicle’s UM, your own UM, or a resident relative’s UM under Fla. Stat. § 627.727.

How long do I have to file a lawsuit?

Generally two years from the crash for negligence claims arising on or after March 24, 2023, under Fla. Stat. § 95.11 as amended by HB 837. Government claims involve additional pre-suit notice. Confirm your specific deadline with an attorney.

Will a claim financially ruin my friend who was driving?

Almost never. Their insurer defends and pays within policy limits — that’s what the coverage is for. Personal exposure typically becomes an issue only when damages exceed limits, which is a scenario your attorney plans around using UM and other coverage layers.

What if several passengers were injured in the same crash?

All bodily injury claims share the policy’s per-accident limit. Acting quickly and identifying every additional coverage source is critical before the shared pool is exhausted.